REGENERON PHARMACEUTICALS (NASDAQ:REGN) Screens as a Top Value Stock with Strong Fundamentals

In the world of investing, value strategies focus on identifying companies trading below their intrinsic worth, often using quantitative screens to filter for strong fundamentals at reasonable prices. The “Decent Value” screen used here emphasizes stocks with high valuation ratings, indicating they may be priced below their true value, while maintaining solid scores in profitability, financial health, and growth. This method agrees with value investing principles by seeking financially sound businesses that the market may have overlooked or undervalued, offering potential opportunities for long-term capital appreciation.

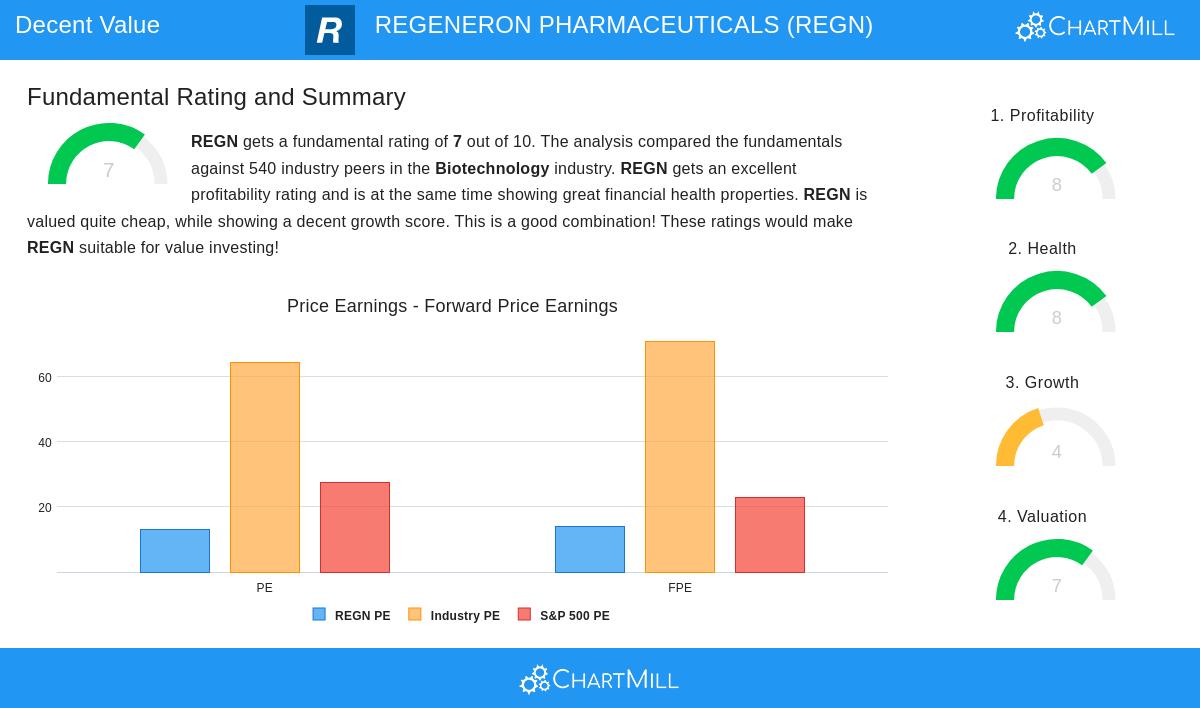

Valuation Metrics

REGENERON PHARMACEUTICALS (NASDAQ:REGN) stands out with a valuation rating of 7 out of 10, signaling that the stock may be attractively priced relative to its fundamentals. Key metrics supporting this view include:

- A Price/Earnings (P/E) ratio of 12.97, notably lower than the industry average of 64.32 and the S&P 500 average of 27.38, placing it cheaper than 96% of its biotechnology peers.

- A Price/Forward Earnings ratio of 14.00, which is below both the industry and broader market averages, reinforcing the stock’s undervalued status.

- Strong Enterprise Value to EBITDA and Price/Free Cash Flow ratios, each performing better than over 95% of industry competitors, suggesting the market may not be fully pricing in the company’s cash-generating ability.

These valuation characteristics are important for value investors, as they indicate a potential margin of safety, a buffer between market price and intrinsic value that can protect against estimation errors or market volatility.

Financial Health

The company’s financial health rating of 8 reflects a strong balance sheet and low financial risk, essential for value investors who prioritize stability and downside protection. Highlights include:

- An Altman-Z score of 6.97, indicating no near-term bankruptcy risk and performing better than 79% of the industry.

- A low Debt-to-Equity ratio of 0.09, showing minimal reliance on borrowing, supported by a strong Debt-to-Free Cash Flow ratio of 0.76, meaning it could pay off all debt in under a year.

- Healthy liquidity with a Current Ratio of 4.60 and Quick Ratio of 3.93, ensuring ample short-term financial flexibility.

Such solid health metrics reduce the risk of value traps, where a stock appears cheap but faces underlying financial distress, making Regeneron a more reliable candidate for a value-oriented portfolio.

Profitability Strength

With a profitability rating of 8, Regeneron demonstrates exceptional earnings power and operational efficiency, key factors that value investors associate with high-quality undervalued companies. Notable points include:

- A Profit Margin of 31.37%, ranking in the top 4% of the biotechnology sector, coupled with an Operating Margin of 28.56% (top 4%) and Gross Margin of 86.46% (top 11%).

- Strong returns on assets (11.67%) and equity (14.89%), each performing better than over 94% of industry peers, indicating effective use of capital.

- Consistent profitability over the past five years, with positive earnings and operating cash flow annually, highlighting business resilience.

High profitability not only supports the company’s intrinsic value but also provides a cushion during economic downturns, aligning with the value investing emphasis on durable competitive advantages.

Growth Considerations

Although growth is rated at a moderate 4, Regeneron shows respectable historical expansion with some slowing in forward estimates, which is common in mature value plays. Key growth aspects include:

- Revenue growth averaging 12.55% annually over recent years, though expected to moderate to around 5% going forward.

- Earnings Per Share (EPS) growth of 13.12% historically, with projections near 5.6% annually, reflecting a shift toward steadier, albeit slower, expansion.

- While growth is decelerating, the company’s established market position and profitability suggest it can still create value, even at a reduced pace.

For value investors, sustainable, rather than explosive, growth is often sufficient, especially when combined with deep valuation discounts and strong financials, as it reduces the risk of overpaying for future expectations.

Conclusion

REGENERON PHARMACEUTICALS presents a strong case for value investors, blending an undervalued price tag with excellent profitability, very solid financial health, and reasonable growth. The stock’s low P/E ratios, high margins, and strong balance sheet suggest it may be trading below its intrinsic value, offering a potential margin of safety. While growth is moderating, the company’s established products and healthy cash flows provide stability, reducing the risk of a value trap.

For investors interested in exploring similar opportunities, additional stocks matching this “Decent Value” criteria can be found using this predefined screen.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making any investment decisions.