How Africans Use Stablecoins to Beat Inflation in 2025

Key takeaways:

-

Stablecoins are now everyday tools for savings, payments and trade in Nairobi and Lagos.

-

Inflation, FX swings and high remittance costs drive adoption.

-

Mobile money links make stablecoins feel familiar and practical.

-

Risks remain around reserves, scams and shifting regulations.

On a Tuesday morning in Nairobi, Amina invoices a client in Berlin. By the afternoon, USDC has landed in her wallet, and within minutes, she cashes out to M-Pesa. What once felt experimental is now routine, thanks to services like Kotani Pay that tie stablecoins to mobile money.

Across the continent in Lagos, Chinedu runs a small shop and keeps his working capital in Tether’s USDt. Holding “digital dollars” means he can restock imports without watching his margins vanish to the naira’s volatility.

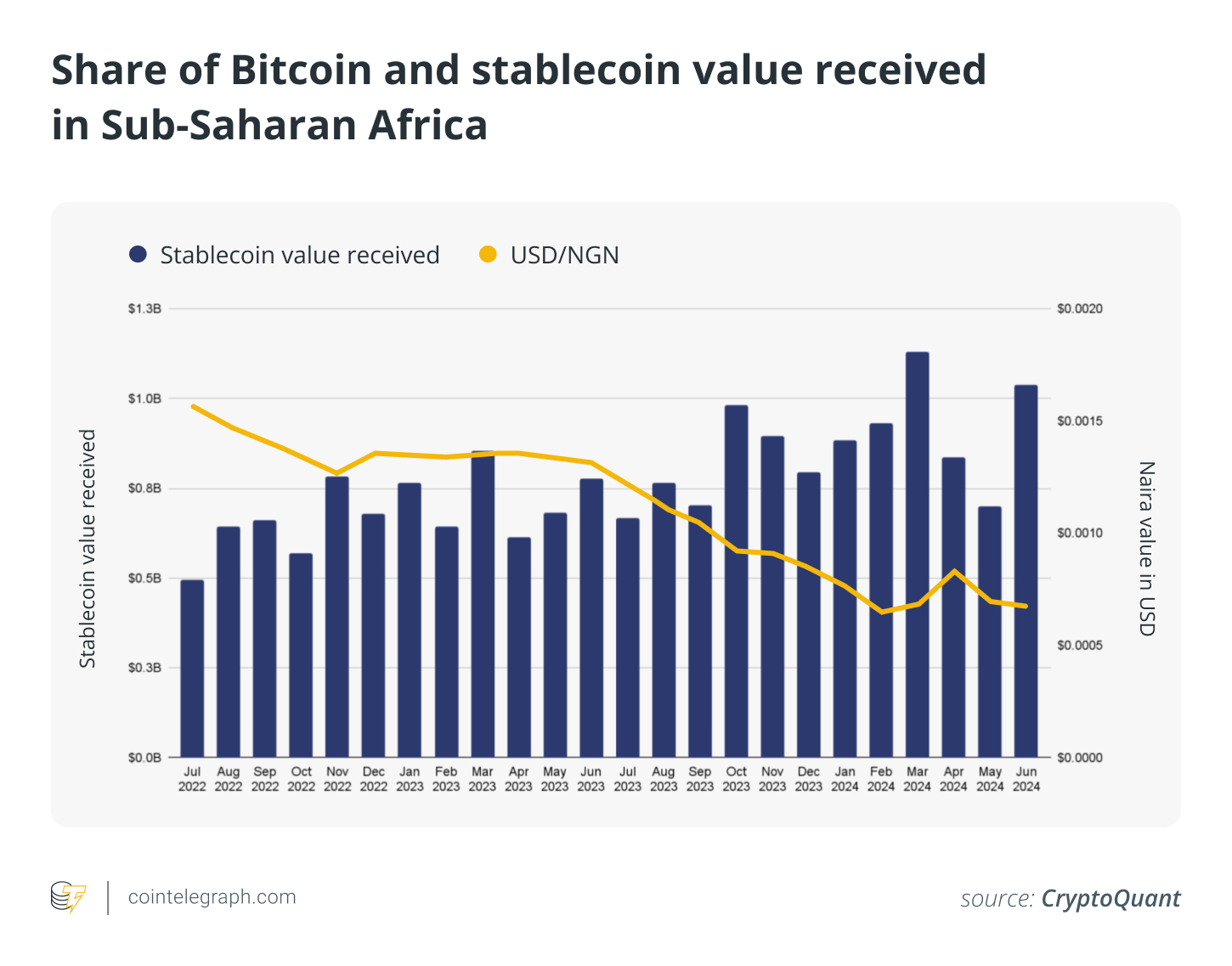

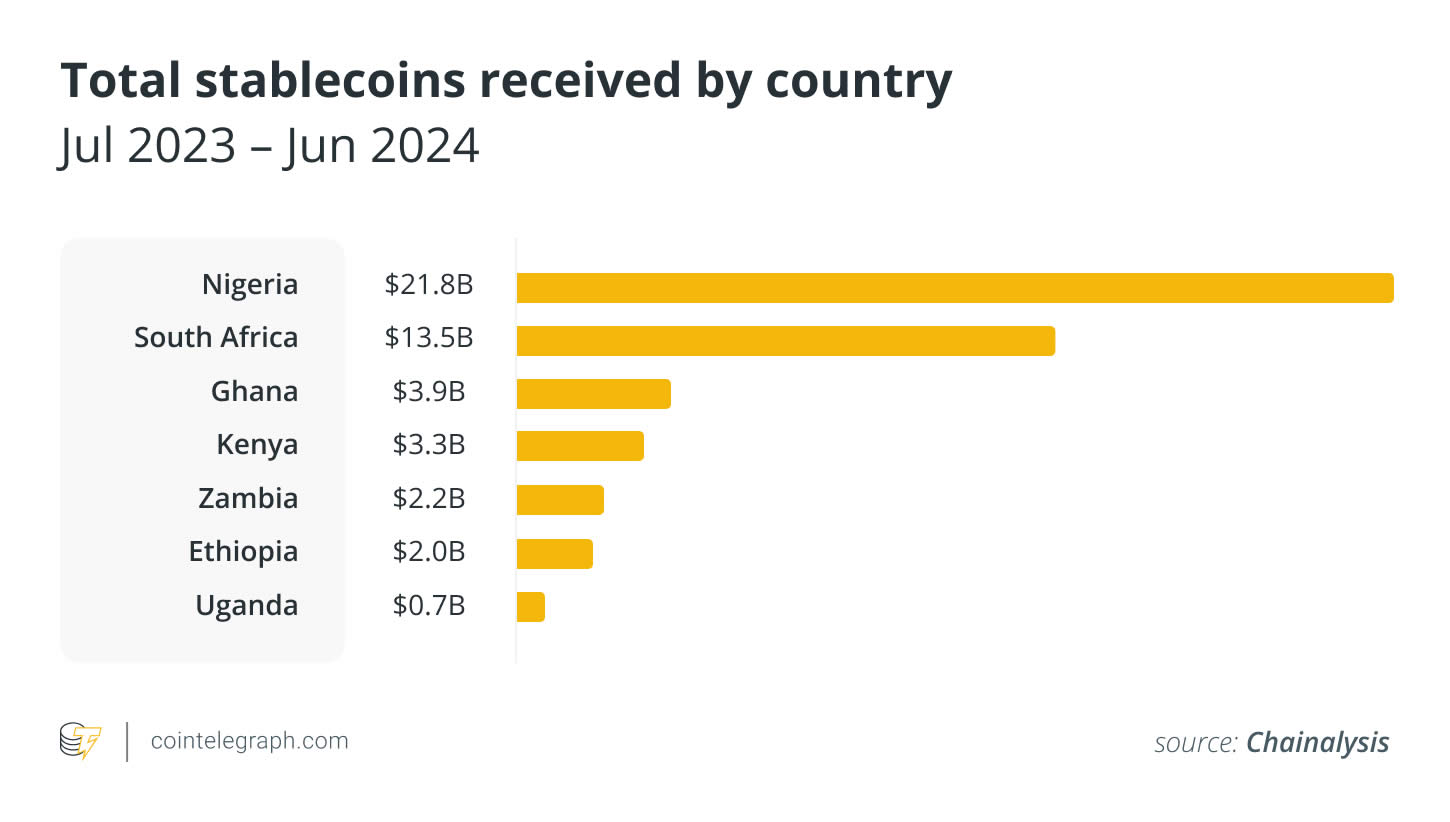

He is hardly an outlier. Between July 2023 and June 2024, Nigeria alone processed nearly $22 billion in stablecoin transactions — by far the largest volume in Sub-Saharan Africa.

The draw is economic. Sending money into the region through traditional remittance channels still costs an average of 8.45% (Q3 2024), while digital-first operators have brought fees closer to 4%.

Add in a stablecoin hop and a reliable cash-out option, and the savings grow sharper, especially on the $200-$1,000 transfers that sustain families and small businesses.

Costs vary by market, but the principle holds: For millions navigating inflation, currency controls and the world’s priciest remittance corridors, stablecoins offer a way to hold value and move money with little more than a phone.

The macro squeeze: Inflation, FX and remittance friction

Nigeria’s cost-of-living crisis hasn’t disappeared. Inflation has eased from early-2025 highs but remains punishing, with the headline consumer price index (CPI) at 21.88% in July 2025, well above target and steadily eroding purchasing power.

Currency reforms since 2023, including multiple devaluations and a shift toward a more market-driven FX regime, have only heightened short-term volatility for households and importers who price necessities in dollars.

Kenya’s picture is milder but follows the same pattern. Inflation ticked up to 4.5% in August 2025, driven by rising food and transport costs, while the shilling’s swings kept USD demand high among traders.

On top of this is the world’s most expensive remittance corridor. The World Bank’s Remittance Prices Worldwide reports show Sub-Saharan Africa averaging 8.45% in Q3 2024, well above the UN’s 3% Sustainable Development Goals target and higher than the global average of 6%.

For families sending $200-$500 at a time, those costs can be the difference between paying rent on time and falling behind.

These pressures explain why stablecoins have become a practical solution for freelancers, traders and small businesses from Nairobi to Lagos.

Did you know? Nigeria’s diaspora sent about $19.5 billion home in 2023 — around 35% of all remittances to Sub-Saharan Africa.

Why stablecoins? The practical economics

For people earning across borders or saving in weak local currencies, stablecoins act as “digital dollars” with two clear advantages: Transfers are clear around the clock, and fees are often lower than traditional money services (especially for cross-border payments).

That mix of speed and affordability explains much of their traction in emerging markets.

In Sub-Saharan Africa, this is already visible on the ground. Chainalysis data shows stablecoins now make up the largest share of everyday crypto activity.

In Nigeria alone, transactions under $1 million were dominated by stablecoins, adding up to nearly $3 billion in Q1 2024. Across the region, stablecoins account for roughly 40%-43% of total crypto volume.

Tether’s USDt (USDT) and USDC (USDC) remain the leading options. At the edge where cost decides behavior, Tron has emerged as a preferred network for moving USDT; by mid-2025, it carried the largest share of USDT’s supply. The logic is simple: People follow whatever option is cheapest and most reliable.

How it works on the ground

On-/off-ramps and P2P

In Kenya and Nigeria, most people get USDT or USDC through a mix of regulated fintechs and peer-to-peer (P2P) marketplaces, then cash in or out via banks or mobile money.

Yellow Card, active in about 20 African countries, runs most of its transfers in USDT. Its Yellow Pay service connects users across borders and supports local cash-outs, including mobile money. Today, stablecoins make up 99% of Yellow Card’s business.

Mobile money bridges

In East Africa, the backbone is M-Pesa and other mobile wallets. Kotani Pay provides conversion services that let partners settle in stablecoins and pay directly into M-Pesa.

Mercy Corps’ Kenya pilot used Kotani to test USDC-to-M-Pesa savings. The flow is straightforward: receive in USDC, convert to shillings and spend through the same wallet people already use.

Fintech scale-ups

Some companies keep the crypto layer invisible. Chipper Cash, for example, uses USDC behind the scenes to move dollars instantly across its network. It has also started using Ripple’s technology to bring funds into nine African markets. For customers, it feels like a faster, cheaper version of a familiar wallet.

Everyday use cases

-

Savings: Converting small balances into digital dollars to protect against inflation.

-

Payroll and gigs: Freelancers and creators often get paid in USDC, converting only what they need into local currency.

-

Trade and inventory: Small and medium-sized enterprises settle invoices and pay suppliers in stablecoins; Yellow Card cites business payments among its fastest-growing segments.

-

Remittances: Stablecoin transfers with local cash-out options often beat traditional remittance services, especially on $200-$1,000 transfers.

Mobile money is already everywhere, with more than 2 billion registered accounts globally. Sub-Saharan Africa sits at the center of this trend.

Regulation and policy drift

Nigeria

The regulatory stance has shifted sharply in recent years, from prohibition to cautious permission, and now toward stricter policing.

In December 2023, the Central Bank of Nigeria lifted its banking ban and allowed banks to open accounts for virtual-asset service providers (VASPs).

But, in 2024, the tide turned again: Authorities cracked down on naira P2P venues and Binance, detaining executives, halting naira pairs and warning of additional rules against illicit trading.

Cases and disputes have continued into 2025. Meanwhile, Nigeria’s Securities and Exchange Commission updated its crypto framework in January 2025, and the new Investment and Securities Act (ISA 2025), now law, clarified registration duties for digital-asset firms. More licensing, disclosure and marketing scrutiny are expected.

Kenya

The Finance Act 2023 introduced a 3% Digital Asset Tax, upheld by the Supreme Court in late 2024.

But policy shifted again in mid-2025. The Finance Act 2025 repealed the levy and replaced it with a 10% excise duty on fees charged by virtual-asset providers. Users and operators now need to track excise, VAT/DST and reporting obligations.

Ultimately, frameworks are evolving quickly. Always check the latest local guidance before choosing a provider.

Did you know? About one in six Kenyan adults lacks any formal financial account. As of 2021, formal financial inclusion reached 83.7%, meaning 11.6% of adults remained entirely excluded from both formal and informal financial services.

The risk ledger

Stablecoins may solve problems of speed and cost, but they carry risks of their own, which fall into three main categories.

Peg and counterparty

Stablecoins are only as reliable as the reserves and governance behind them. The Bank for International Settlements and the International Monetary Fund analyses warn that rapid growth could trigger financial-stability issues, from forced sales of reserve assets to “dollarization” that undermines local monetary control.

The USDC de-peg in March 2023 showed how quickly confidence shocks can spread. Independent reviews have also flagged transparency gaps and issuer concentration as ongoing concerns.

Operational

On the ground, everyday risks include P2P scams, wallet theft, bridge failures and difficulties cashing out.

Regulatory actions can make matters worse. Nigeria’s crackdown in 2024-2025 froze accounts and stranded balances overnight, illustrating how suddenly access can disappear.

Policy

At a systemic level, heavy reliance on dollar-linked stablecoins can accelerate informal dollarization and shift payments outside regulated banking channels. In response, policymakers are pushing for tighter licensing, stricter reserve standards and more disclosure from issuers.

Did you know? At the 2025 Stablecoin Summit in Lagos, SEC Director-General Emomotimi Agama declared, “Nigeria is open for stablecoin business, but on terms that protect our markets and empower Nigerians.”

What comes next for stablecoins in Africa?

Stablecoins won’t solve inflation or rewrite FX policy, but they already make saving, getting paid and sending money across borders cheaper and faster for many in Nairobi, Lagos and beyond. Their integration with mobile money is what makes them feel practical.

Builders frame stablecoins as tools for everyday utility, while regulators worry about dollarization and financial stability. The balance between those forces will shape what comes next.

On the ground, the safest approach is straightforward: Keep costs low, stick with trustworthy providers and stay alert as rules evolve.

What’s likely ahead is clearer disclosure requirements, tougher licensing and more “crypto in the background” services, where users don’t see tokens at all, just value moving instantly and at a lower cost.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.